Published 14 Oct 2022

560,000 car finance customers have been overpaying by £300m annually, estimates UK financial regulator.

Research

Group Actions

560,000 car finance customers have been overpaying by £300m annually, estimates UK financial regulator.

A 2019 FCA report found that some customers were being overcharged more than £1,000 in interest charges.

This report continues to gain attention, as potential consumer claims against finance lenders build momentum.

Here are 5 key takeaways:

1. "...the way commission arrangements are operating in motor finance may be leading to consumer harm on a potentially significant scale."

2. "...we estimate that commission models which allow broker discretion over the interest rate could be costing customers £300m more annually when compared against a baseline of Flat Fee models.

3. "The difference between the average and highest commission was around £2,000 for the DiC [Difference in Charges] and Scaled models, compared to £700 for the Flat Fee commission model."

4. "We estimate that on a typical motor finance agreement of £10,000, higher broker commission under the Reducing DiC model can result in the customer paying around £1,100 more in interest charges over the four-year term of the agreement."

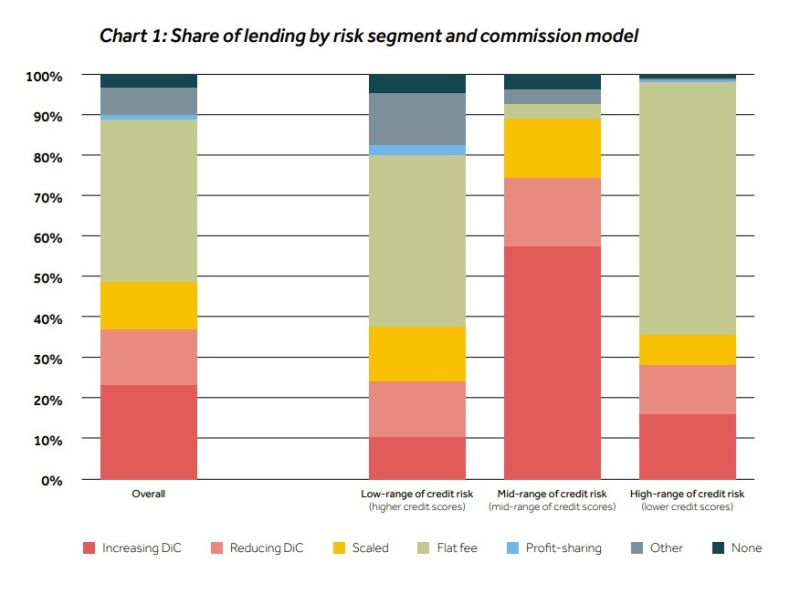

5. "Difference in charges models (Increasing and Reducing) were more prevalent in the mid-range of credit risk, accounting for around 75% of lending within that segment." [See image]

On January 28, 2021, the FCA introduced new rules to prohibit the discretionary commission model for regulated credit agreements.

Christopher Woolard, the FCA’s Interim Chief Executive, said:

"We estimate that consumers could save £165 million because of today’s action."

A link to the report is here: https://www.fca.org.uk/publication/multi-firm-reviews/our-work-on-motor-finance-final-findings.pdf

Read the full LinkedIn post by James Jackson, Managing Director here:

Recent Posts

Published 14 Oct 2022

560,000 car finance customers have been overpaying by £300m annually, estimates UK financial regulator.

Research

Group Actions

560,000 car finance customers have been overpaying by £300m annually, estimates UK financial regulator.

A 2019 FCA report found that some customers were being overcharged more than £1,000 in interest charges.

This report continues to gain attention, as potential consumer claims against finance lenders build momentum.

Here are 5 key takeaways:

1. "...the way commission arrangements are operating in motor finance may be leading to consumer harm on a potentially significant scale."

2. "...we estimate that commission models which allow broker discretion over the interest rate could be costing customers £300m more annually when compared against a baseline of Flat Fee models.

3. "The difference between the average and highest commission was around £2,000 for the DiC [Difference in Charges] and Scaled models, compared to £700 for the Flat Fee commission model."

4. "We estimate that on a typical motor finance agreement of £10,000, higher broker commission under the Reducing DiC model can result in the customer paying around £1,100 more in interest charges over the four-year term of the agreement."

5. "Difference in charges models (Increasing and Reducing) were more prevalent in the mid-range of credit risk, accounting for around 75% of lending within that segment." [See image]

On January 28, 2021, the FCA introduced new rules to prohibit the discretionary commission model for regulated credit agreements.

Christopher Woolard, the FCA’s Interim Chief Executive, said:

"We estimate that consumers could save £165 million because of today’s action."

A link to the report is here: https://www.fca.org.uk/publication/multi-firm-reviews/our-work-on-motor-finance-final-findings.pdf

Read the full LinkedIn post by James Jackson, Managing Director here:

Recent Posts

Supercharge your Client Onboarding

Join the law firms automating their customer experience.

Supercharge your Client Onboarding

Join the law firms automating their customer experience.